Apr 4, 2023

With spring upon us, many home sellers could be wondering: Should I sell my home now?

While this season tends to bring out both home sellers and buyers en masse, this particular spring is prompting many to pause.

For one, sellers have all heard the stories of how, just a year or two earlier, bidding wars and six-figures-over-asking offers were the norm. But now that interest rates have more than doubled in the past year, financially hampering both buyers and sellers alike, this insane seller’s market seems to be over. Understandably, some home sellers are kicking themselves for not listing during its heyday.

And since most sellers also become buyers, many are hesitant to give up their low mortgages and enter into the fray of today’s stressed housing market.

As a result, many would-be home sellers are taking more of a wait-and-see approach rather than jumping into the market. In March, there were 20.1% fewer homes listed for sale than at this same month last year. Meanwhile, the Fannie Mae Home Purchase Sentiment Index found that the share of home sellers who believe now is a good time to sell is down annually by 18%.

Yet despite the pessimism looming over the prospect of selling this year, the latest housing data suggests the outlook isn’t as bad as many might think.

If you’re a homeowner who’s trying to decide whether to list your home this season, here are some reasons why it might make sense to take the plunge now—and a few instances in which it could be better to wait.

Reasons to sell a house now

Even though sellers might not see the insane bidding wars and packed open houses they saw a year or two earlier, make no mistake, the market still favors sellers. Some reasons:

Home prices are still rising

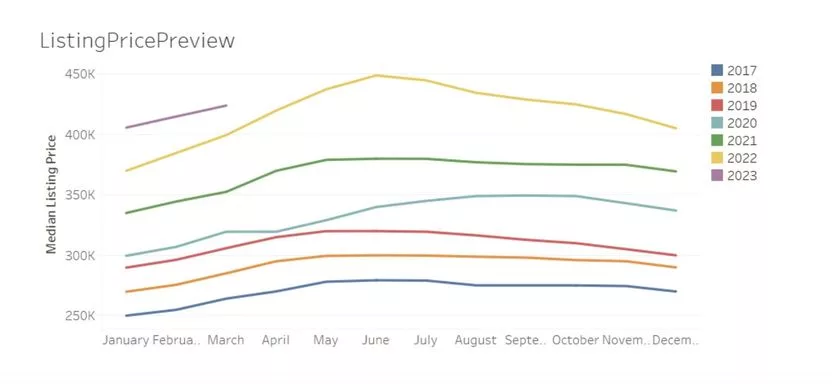

Back in June, U.S. median home prices reached an all-time record high of $450,000, and some home sellers might be admonishing themselves for missing the peak.

The reality, though, is that home prices are highly cyclical, declining during the wintry off-season then swinging upward in the spring. As such, although listing prices bottomed out at $406,000 in January, they’ve been creeping upward since then, reaching $424,000 in March.

Plus, home prices are still up from last year. In February, the median list price was 6.3% higher than this same month last year. And the longer you’ve owned your home, the bigger the gains. Back in 2017, home prices hovered well below $300K (see chart below to get an idea of how much listing prices have appreciated).

As for what home prices will do next—that remains to be seen, although there is plenty of reason to remain hopeful.

“Most other forecasts call for price declines,” says Danielle Hale, Realtor.com® chief economist. “But that’s not what we’re expecting.”

Home equity is at all-time highs

Homeowners who’ve been paying their mortgage month to month should take heart that they’ve likely built up a considerable amount of home equity—the difference between the current value of a home and how much is owed on the mortgage. In fact, recent surveys suggest that nationwide homeowner equity levels have risen to 70%, a near-40-year high.

Let’s presume, for a moment, that you’re one such homeowner, with 70% equity in a house currently worth $400,000. This would mean that when you sell, you’d walk away with $280,000 (minus closing costs and commission, of course). This puts you in a powerful position, in that this windfall could be put toward buying a new home—perhaps in all cash or close to it.

“Now is a good time to be a cash buyer,” says Hale. “If you’re a homeowner lucky enough to have paid down your mortgage considerably or you own the home outright, then mortgage is less of a factor for you.”

In addition to bypassing today’s high rates, all-cash or high-cash offers can help your offer on a new house stand out. It can even give you added negotiation muscle to get a good deal in a market where few buyers can stomach the high mortgage rates. As Hale says, “You might benefit from the lack of competition.”

Curious to find out how much equity you have in your home? Check out Realtor.com’s online mortgage calculator or online estimates of how much your house is worth.

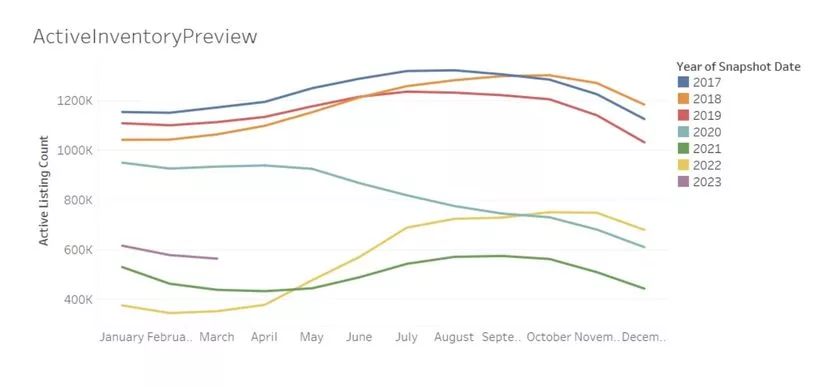

The supply of homes is at rock-bottom lows

It’s hard to remember what selling a home was like before the COVID-19 pandemic. But here’s a reminder of just how different things are today.

“Nationwide, there are just a bit more than half as many homes for sale as were available pre-pandemic,” says Hale.

Part of the reason for this is that people are living in their homes longer; baby boomers who may have downsized in the past are staying put. As a result, homebuyers really just don’t have the selection they used to—and the listings that are up have been lingering longer, growing stale.

This means that any new listings are bound to get a lot of attention, which bodes well for any sellers dipping their toe in the market.

A variety of sales methods offers sellers flexibility

Traditionally, the process of selling a house involved weeks or even months of time and effort, prepping a place and fielding offers from buyers. Today, though, home sellers have a wide variety of options to consider that make home selling much easier, faster, and more flexible than it was in the past.

One option is to get what’s called an “instant offer” from an ibuyer, a company that can pay for a house in all cash. Ibuyers will typically buy a house fast, in any condition, and give sellers the freedom to remain in their home until they’ve found a new place to purchase. While these companies do charge a fee, the convenience may be worth it to many sellers who want to avoid the headaches of a more traditional sales process. Here’s where you can learn more about the various ways to sell a house.

More buyers will get out there as the weather warms up

Whatever mortgage rates do, buyers tend to come out in force in the spring. So you’ll get a lot more interest in your home, particularly from people who might be more serious about buying. In fact, Realtor.com has determined that the very best time to sell for 2023 is the third week in April, when listings are expected to receive 16% more views than in a typical week and fetch $8,400 more per sale.

There are some caveats to this approach, however. As Thai Hung Nguyen, a real estate agent with Better Homes and Gardens in Falls Church, Virginia, puts it, if there are more house hunters out on the market, there will be more homeowners deciding to list, so you’ll have more competition.

“Pick your battle,” Nguyen advises.

Nobody knows what mortgage rates will do next

It’s impossible to accurately predict whether mortgage rates will go up or down—and if they go up, when or by how much. That’s why Steve Reese, a real estate agent with NextHome Central Real Estate in Shawnee, OK, says, “I don’t ever promise someone that rates will go down.”

In other words, don’t get yourself into a situation where you’re delaying life decisions based on where the market might be expected to go. Base your decisions on the here and now—and your own needs.

It’s the right time for you, personally

No matter what interest rates and home prices do next, sometimes homeowners just have to move—due to a new job, new baby, divorce, death, or some other major life change.

Nguyen has been working with a retired couple to sell their home and relocate to Florida, a goal they’ve been ready to implement for years.

“They were debating, ‘Did we miss the market?’” Nguyen says. “When they decided to relocate, the decision seemed to be easier for them because they had their mind set on it, versus those people who just think, ‘Maybe I’d like a bigger home.”

Hale agrees, noting that there are various situations in which it might not be the right time to buy or sell, market-wise; but it is the right time, given a buyer’s particular situation or needs.

“In all cases,” says Reese, “the decision to move and the home that you end up buying is an emotional decision. It’s not usually based on numbers on a spreadsheet. So people generally, if they feel like they need to move or just want something different, they’re going to make it work.”

Bottom line? Don’t hold off on important life decisions purely because you’re trying to time the market and wait for a better deal, or because can’t sell your home for as high a price as your neighbors down the block did last year. The right time to sell is not just about money.

Reasons to hold off on selling your house

For all the reasons why it might make sense to sell right now, there are a few considerations that suggest you might be better off waiting.

You need a new (large) mortgage

If you haven’t lived in your home all that long, and you haven’t made much of a dent in your mortgage, any transaction expenses will probably wind up costing you dearly. Think real estate agent commission, closing costs, expenses incurred making preparations and repairs, and so on.

And if this describes you, and you are selling in order to buy, you might get sticker shock when you compare your current mortgage payment to a new one. Rates may be double or more what you’re paying now, and home prices are pretty high, too. This amounts to a mortgage payment averaging around 50% more than only a year earlier.

Your house needs a lot of work

High mortgage rates have had another peculiar impact on buyers: Since they’re paying more for the house, they want it to be perfect—“more than move-in ready,” as Nguyen puts it. “The buyer mentality right now is, ‘I have to pay a lot because of higher prices and higher rates, I expect more.’”

That could mean putting some work into your house before listing it … or resigning yourself to accept a lower sale price than you might have wanted.

You’d like to move but don’t have to

Yes, you are in a good position as a seller. But if you are selling in order to buy, and you don’t know if that next home is out there, you might be better off just sparing yourself the ordeal.

That’s the approach of Seattle homeowner Kevin Kim. He and his wife bought a nice home in 2018, then had a baby a few years later. Kim calls moving to a bigger place “definitely more of a want than a need.”

The couple bid on one home that Kim really liked but were outbid, and they’re okay with that.

“We’ve looked at other places, but it’s a huge process,” says Kim. “There’s a lot of stuff that goes into trying to move, especially when the market is shifting.”

Source- https://www.realtor.com/advice/sell/should-i-sell-my-house-now-reasons-to-list-times-to-wait/